Mid-September 2025 Northern Virginia Real Estate Market Update | New Listings Increase, New Contracts Flat, While Inventory & Days on Market Remain High

- Scott Ford

- Sep 19, 2025

- 6 min read

Updated: Oct 9, 2025

How is the Northern Virginia real estate market in mid-September? Has the expectation of the Federal Reserve's interest rate cut at the September meeting this week affected our Market activity?

Let's get the answers through a deep dive look at the Buyer Activity Level measured by New Contracts, Days on Market, and Inventory of Houses for sale.

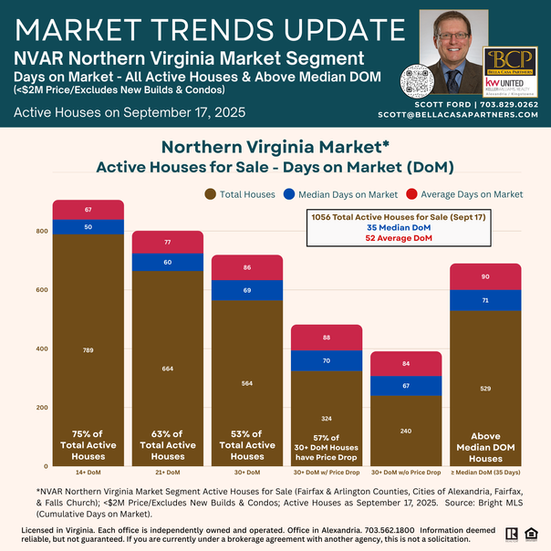

📸 Market Snapshot: The higher Active Listing Inventory during the Spring and Summer months continues into September, which means more options for Buyers, who are taking longer to make a decision on a house than 2024. More options & a longer time to act means continued upward pressure on Days on Market (DoM), which is why we see an increasing DoM over the past two months, even as the level of Buying activity through August is on par with 2024.

Buyers currently have more leverage - coupled with Mortgage rates testing the lowest rates over the last 2 years - than they have had in 2023 or 2024.

I provide a Market Summary below, but read the full Post for all the details.

Each chart in the Post is also included below for ease of data viewing.

At the start of 2025, I began tracking New Contracts activity in Fairfax County for the first half/second half of each month, with a comparison to 2024 and 2023 Contract activity. This tracking provides real time insight into the Buyer activity trend, especially when compared to the increase in Days on Market data as the Spring 2025 market progressed. As the largest market in NoVA, Fairfax County is a good barometer of the Overall NoVa market.

➡️ New Contracts in 1st Half of September were flat to the 2nd Half of August, but up slightly (+5%) to the same period in 2024.

➡️ Buying activity (measured by New Contracts) in Fairfax County during 2025 through August is on par with to 2024 (just 32 fewer Contracts in 2025).

➡️ New Listings in Fairfax County are up only slightly in 2025 through August (+2.5% vs 2024/just 214 more Listings over 8 months), with New Listings in May through August slightly trailing 2024.

➡️ The Northern Virginia market segment* also has a similar small deviation to 2024, with just 4% more New Listings through August. New Contracts in the NoVA market segment are up just 1.1% in 2025 through August versus 2024 (130 more Contracts in 2025 over 8 months). *The Northern Virginia market segment in the Northern Virginia Association of Realtors data includes Arlington & Fairfax Counties and the Cities of Alexandria, Fairfax, & Falls Church.

➡️ Active Listings* for Sale have increased across all NoVA localities by a significant % in March through August compared to 2024. Fairfax County had 31% more Active Listings versus August 2024, which follows increases of 62%, 46%, 50%, & 40% in April through July. Based upon the increase in New Listings during the first two weeks of September compared to 2024 & New Contracts running less than the New Listings so far this month, September is likely to continue this % increase trend for Active Listings. *The Active Listing category includes all properties that were Active for Sale during the month. As houses stay on market longer, a house might be an Active Listing for 2-4 consecutive months, whereas the same house in 2024 would list and go under contract within 1 month.

➡️ The DoM numbers show that the Buyers continue to have a lengthy house decision process. The Active for Sale Houses on September 17 in Fairfax County have a Median & Average DoM of 34 & 50 days. The 50% of Houses for Sale above the Median DoM have an average 84 days on market. The overall Northern Virginia market segment has similar DoM numbers (35/52/90 days). The increase in DoM has stabilized at a high level since early July. We saw a slight decrease in DoM numbers over the past two weeks, but this decline is due to the influx of New Listings in Fairfax County, rather than Buyers putting more high DoM houses under contract.

➡️ The DoM numbers for houses going Under Contract in the 1st Half of September continue to show that a house is taking 2-3 weeks longer to get a Contract than the same period in 2024. At present, the Average DoM for a Contract is 28 days. However, if a house does not get a Contract during the first two weeks on market, the data suggests that Sellers face a likely potential for the house to wait a further month or longer. For houses that have more than the 1 month Average DoM, the wait for a Contract could be as long as 2+ months.

➡️ The 2025 Spring Market broke the expected trend by increasing Supply each month, with the amount of Supply now at the highest level in the last two years. The Months of Supply in Northern Virginia during April-July was approximately 2x what we saw in 2024. The Supply number stabilized at just under 2 months during this period. The key question is whether the Supply increases further during September and October consistent with prior years activity.

📢 WHAT'S THE MOST IMPORTANT MARKET NUGGET? 📢

The weekly New Listings vs. New Contracts spread is the best indicator of the real-time market and potential leading indicator of where the Market may be trending.

New Listings are up during the first two weeks of September, back to a level not seen since early July (+19% & +14% vs. same weeks in 2024). For the first Half of September, New Listings outpaced New Contracts (+26%). For most weeks in June through August, New Contracts were higher than New Listings. The spread was not material, so we did not see a reduction in the high Active House for sale Inventory. If New Listings continue to outpace New Contracts during the 2nd Half of September, the Active House for sale Inventory will likely move higher. At a minimum, the Market should remain at the high Inventory level we saw over the Summer months.

WHAT COMES NEXT? 🙋🏼♂️🤔

Does the current data suggest a different level of Buyer activity for the remainder of September into October? Will more Buyers take action now that the Federal Reserve reduced the Fed Funds rate at the September meeting, with the expectation that further reductions will occur at the October and December meetings?

Mortgage rates have moved sharply lower over the past 2-3 weeks in expectation of the Federal Reserve's rate cut plans. We are testing 2-year lows in the 30 Year Conventional & VA Fixed rates. However, the decline in mortgage rates has not - so far - caused more Buyers to act by putting houses Under Contract in September. The weekly Under Contract totals for the 1st Half of September are either below or in line with the totals seen over the prior three months (i.e., at/near 300 New Contracts each week).

We know that Buyers have more houses to choose from with the current higher Inventory level. More choices means a market environment where Buyers have more leverage than we have seen during the past two years. I see nothing in the current data that suggests that the high DoM level we currently have will abate, nor is the high House for Sale Inventory level likely to decline in September unless we get a substantial "overage" of New Contracts vs. New Listings prompted by the Federal Reserve's actions & the current lower mortgage rates. At present, we are just over 2 months of Inventory in the NoVA market, which is double the level seen in the last 5 years. Our market has been locked in a 1 month inventory range for so long that a 2 month supply of Inventory “feels” & “acts” like a Balanced Market.

For for my prior Market Update posts May through July, check out the following links:

See more market news, insight, & analysis on my "How's the Market?" Blog at bellacasapartners.com/marketnews.

Comments